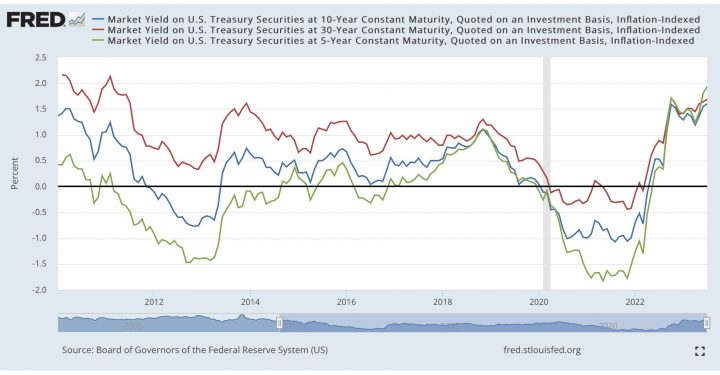

One of my regular bookmarks is the TIPS real yield page (along with the regular Treasury yields). I noticed that the real yield on the 30-year TIPS has nudged above the 2{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} mark:

At the same time, the 30-year regular Treasury is at 4.3{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5}, making the break-even annual inflation rate about 2.3{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5}. Over the next 30 years, I’d take the over on that, or at least take some insurance out on the possibility of high inflation.

In addition, as David Enna of Tipswatch points out, this is the first time in a long while that all the various maturities (5/10/30 year shown below) are all around 2{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5}.

If you wanted to, you can again construct a ladder of TIPS that will provide you a guaranteed inflation-protected income over the next 30 years (including spending down your principal) of over 4{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} above inflation (~4.4{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} as of this writing, as rates are higher today that at the time of writing for that post).

That means if you put $1,000,000 into a 30-year TIPS ladder right now, you can create ~$44,000 income for year 1 and then another ~$44,000 adjusted for inflation (CPI-U) annually for the next 29 years. All fully backed by the US government. No stock market volatility. No chance of annuity insurance company failure. Check out TipsLadder.com and Eyebonds.info if you are ready to get deep into the details.

While I am not looking into investing a lump sum into a TIPS ladder, I do own both regular US Treasuries and TIPS to provide the stable, guaranteed growth portion of my portfolio. (I’m roughly 70{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} stocks and 30{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} bonds.) If I’m getting guaranteed 5{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} growth from US Treasuries and guaranteed 2{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} + inflation from TIPS, I’m pretty happy with that for the safe part of my portfolio.

I am taking this opportunity rebalance my existing bond holdings and free cash to create an overall longer duration for my TIPS. I want to lock in that 2{dec8eed80f8408bfe0c8cb968907362b371b4140b1eb4f4e531a2b1c1a9556e5} real yield across longer maturities while it is available. Real yields might go even higher, but I’m more worried about it going lower than higher.